|

During the 1980s, the Fidelity Magellan Fund returned 21.8% a year to investors. The market was up 16.2% a year, so it was a great time, in general, to be in the market. But the average investor in Fidelity Magellan during the 80s only made 13.4%. So, how is that? How is it that investors did worse than the actual fund?

In short, emotions often drive investor decisions. In one of the more dramatic examples, look to Black Monday, October 19, 1987, when markets crashed on a global scale. Domestically, the Dow fell 508 points (22.61%) in a single day and investors followed suit, selling at the bottom.

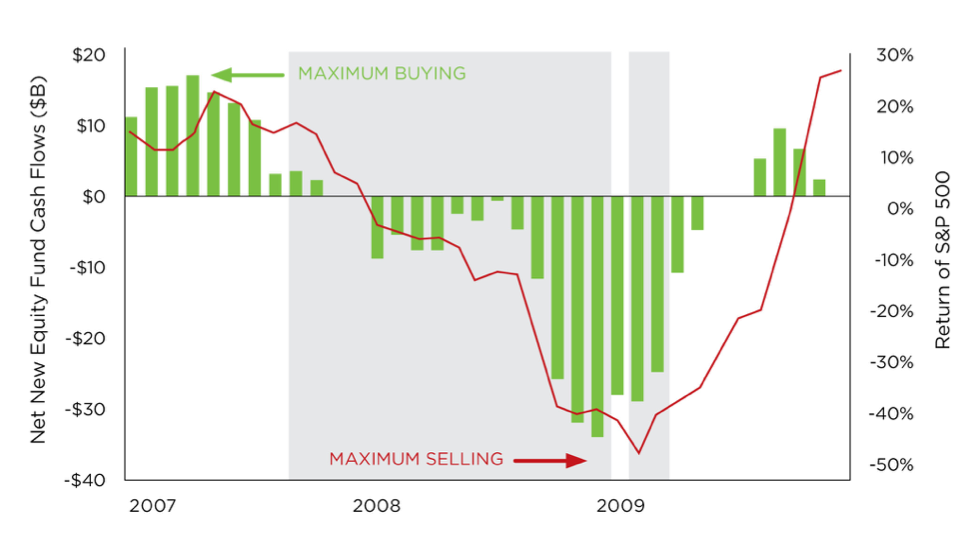

That negative trend of selling at market lows and buying at market highs remains a fixture for emotional investors. More recently, in 2007, as the housing bubbled swelled, we experienced a euphoria from investors. As the S&P 500 reached its peak, so did net new equity fund cash flows as investors bought at the top. Once the bubble burst, so did investor confidence. They sold at the bottom, and in doing so, lost their gains.

In both cases—buying at the top and selling at the bottom—investors made the wrong decision at the wrong time. Why would someone make that choice?

Aversion Diversion

According to behavioral theorists Daniel Kahneman and Amos Tversky, humans, by nature, are loss-averse—they dislike losses more than they enjoy successes. In their studies, Kahneman and Tversky found that people react twice as strongly to losses as to gains. For example, if you give someone a dollar, they register a ten in pleasure; however, if you take a dollar away from someone, they will register a 20 in pain. They further reveal that people are so averse to feeling that pain “they are willing to take risks to avoid the losses.”

Behavioral Coaching

With emotional impulses causing bad decisions for investors, it creates an opportunity for advisors to offer behavioral coaching to their clients. At Beacon, we’ve identified three key components of behavioral coaching.

1. Client education. As we discussed in a recent Bright Ideas column, education is at the forefront of the advisor-client relationship. With an education-first approach, the advisor makes sure the client understands why financial decisions are made, which helps build trust in the advisor and confidence for the investor.

2. Investment alignment. When you work with clients, it’s vital you make sure their investments are aligned with their goals, and the best way to achieve this is by helping them identify and truly understand what their investment goals are. This goes beyond a total number they want to achieve for retirement. It explains how they can get there through mechanical investment models that are based on a balanced portfolio and not reliant on chasing returns.

3. Emotional rescue. One of the most important aspects of behavioral coaching is dealing with the client’s emotional state during the natural market ups and downs. When a client gets panicky during market turmoil or extreme volatility, advisors serve an important role in helping calm them by explaining how their portfolio works and why it’s designed to help capture market upsides, but also to guard against catastrophic losses.

If you would like more information on Beacon’s strategies to help you serve as your client’s behavioral coach, contact your wholesaler today!

* Note – Gray overlay represents BCM’s August 17, 2007 to January 2, 2009 Stop Loss cycle, and BCM’s January 22, 2009 to March 25, 2009 Stop Loss cycle.

Source: Investment Company Institute and Dimensional Fund Advisors, December 12/31/2014

Data: Total return of equities is measured by the rolling 1-year total return of the S&P 500. Net new equity cash flows are measured by the rolling 6-month net cash flows.

|